Scott Barbour

Introduction

Earnings season is heating up, which means we get to enjoy a wave of new data, comments, and other intel when we assess the world's largest corporations.

Yesterday, we discussed one of my all-time favorite companies, RTX Corporation (RTX), which was formerly known as Raytheon Technologies.

The defense giant benefited from massive demand growth in both defense and commercial aerospace, which allows the company to present a very rosy outlook.

In this article, we'll discuss one of RTX's peers, the General Dynamics Corporation (NYSE:GD), one of America's largest defense contracts that also has significant commercial exposure through its Gulfstream business.

The company has hiked its dividend for more than 25 consecutive years, which makes it a dividend aristocrat. It just reported fantastic Q4 earnings.

While Gulfstream G700 certification delays caused a revenue and earnings headwind, the company benefited from the best demand environment in many years, allowing it to present strong guidance and financial results.

My most recent article was written on October 18, when I used the title "General Dynamics: A Top-Tier Dividend Stock With Improving Tailwinds."

In this article, I'll explain what all of this means for the risk/reward and how I would assess the company, which benefits from more than the ongoing demand for defense supplies among NATO and allied nations.

So, let's get to it!

General Dynamics Delivers A Blowout Quarter To End A Terrific Year

For readers who are new to my articles, let me explain that I have more than 25% defense exposure in my dividend portfolio. I own Lockheed Martin Corporation (LMT), RTX Corporation, Northrop Grumman Corporation (NOC), and L3Harris Technologies, Inc. (LHX).

The only reason why I do not own General Dynamics is because I have all bases covered already. I have commercial exposure through RTX, I have "technology" exposure through all of them, and I have combat systems and Navy systems covered through the fact that all of my holdings are suppliers to companies like General Dynamics.

However, if I were running a portfolio of 50 stocks instead of fewer than 25 dividend stocks, I would be an owner of GD as well.

With that said, GD just reported its numbers, which were absolutely fantastic.

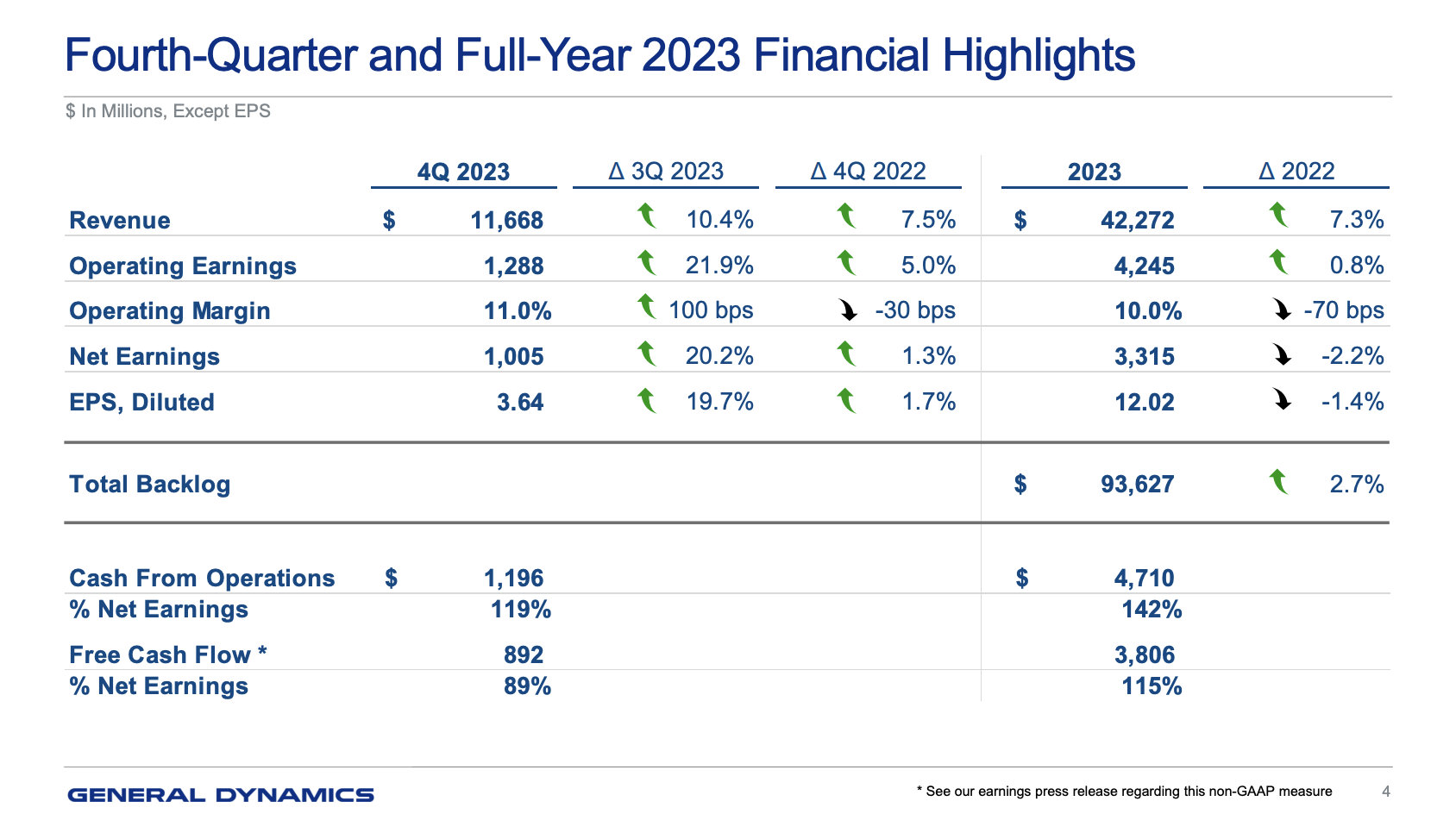

In the fourth quarter of the year we just left, earnings per diluted share came in at $3.64, with revenue reaching $11.7 billion.

Notably, revenue showed a substantial 7.5% increase compared to the same quarter in the previous year.

Operating earnings saw growth as well, rising by $61 million, resulting in a 1.7% increase in earnings per share.

General Dynamics

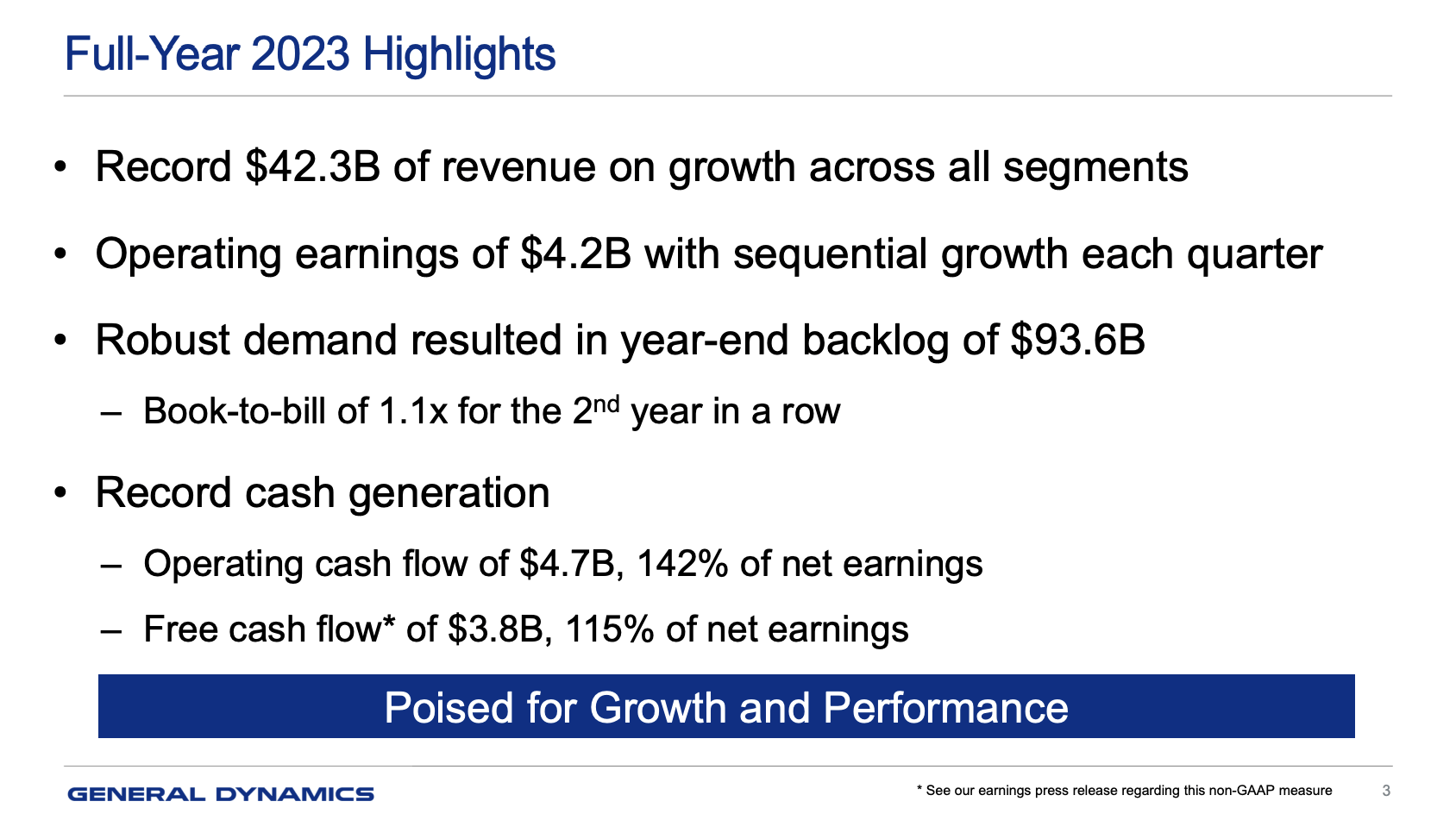

Thanks to this strong performance, annual revenue rose to $42.3 billion, reflecting a significant 7.3% growth.

Operating earnings reached $4.25 billion, marking a 0.8% increase.

Now, before we discuss its outlook, which may be the most impressive thing we'll discuss in this article, let's take a closer look at its segment results.

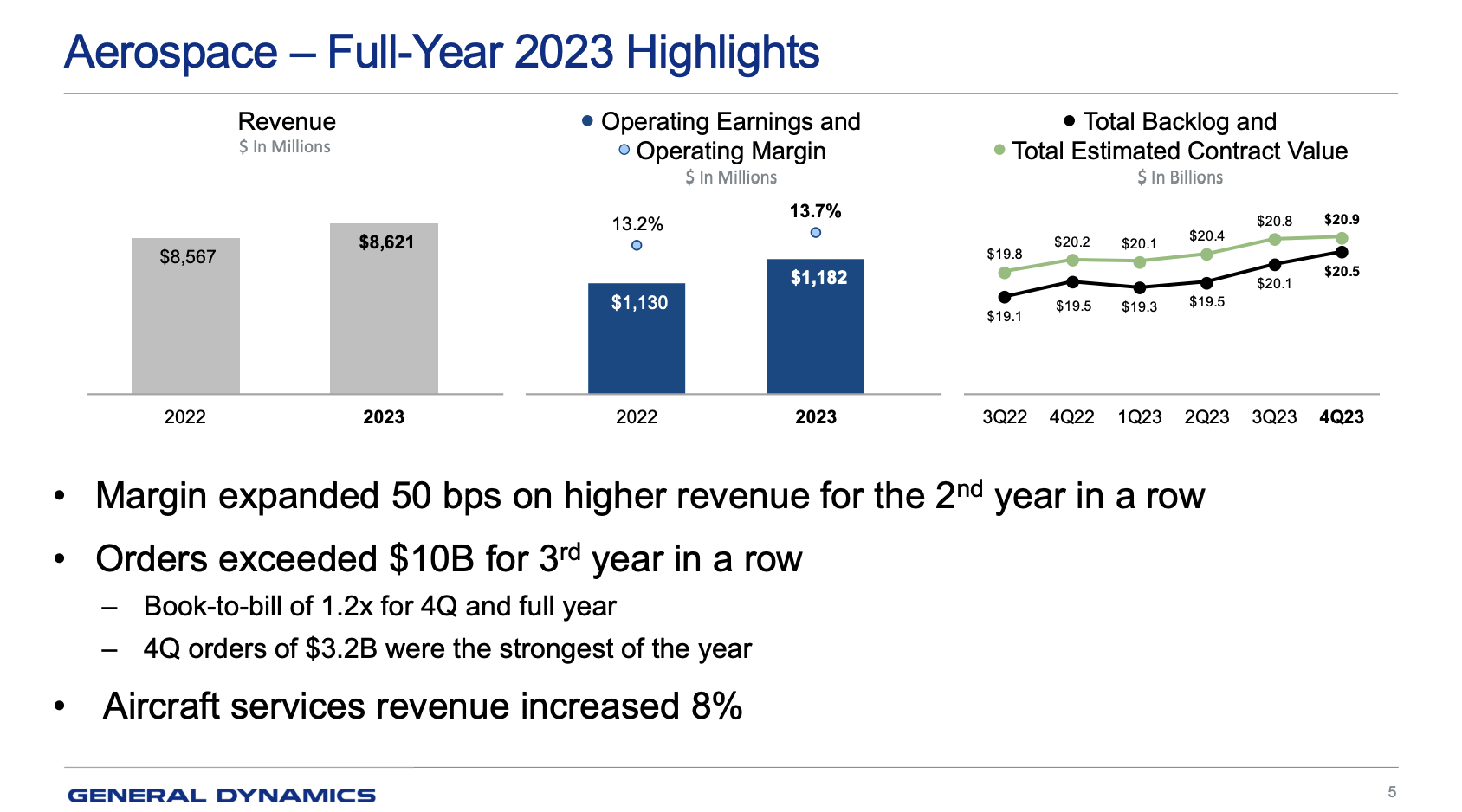

- The aerospace segment showed significant improvements in Q4, marked by a 12% increase in revenue and a substantial 33% surge in earnings on a year-over-year basis. Strong demand for Gulfstream aircraft, coupled with robust Gulfstream service business and Jet Aviation growth, contributed to this positive performance. The quarter also saw a remarkable 35% increase in sequential revenue, accompanied by a staggering 68% boost in operating earnings. Key factors driving this success include a significant uptick in the delivery of in-service airplanes, a favorable mix favoring large aircraft, robust pricing in the backlog, improved overhead absorption, and enhanced supply chain response.

General Dynamics

On a side note, please note that the fourth quarter was significantly impacted by the G700. Gulfstream's flagship did not receive certification, which delays revenue recognition. However, 1Q24 is expected to see certification, which means there's nothing to worry about here.

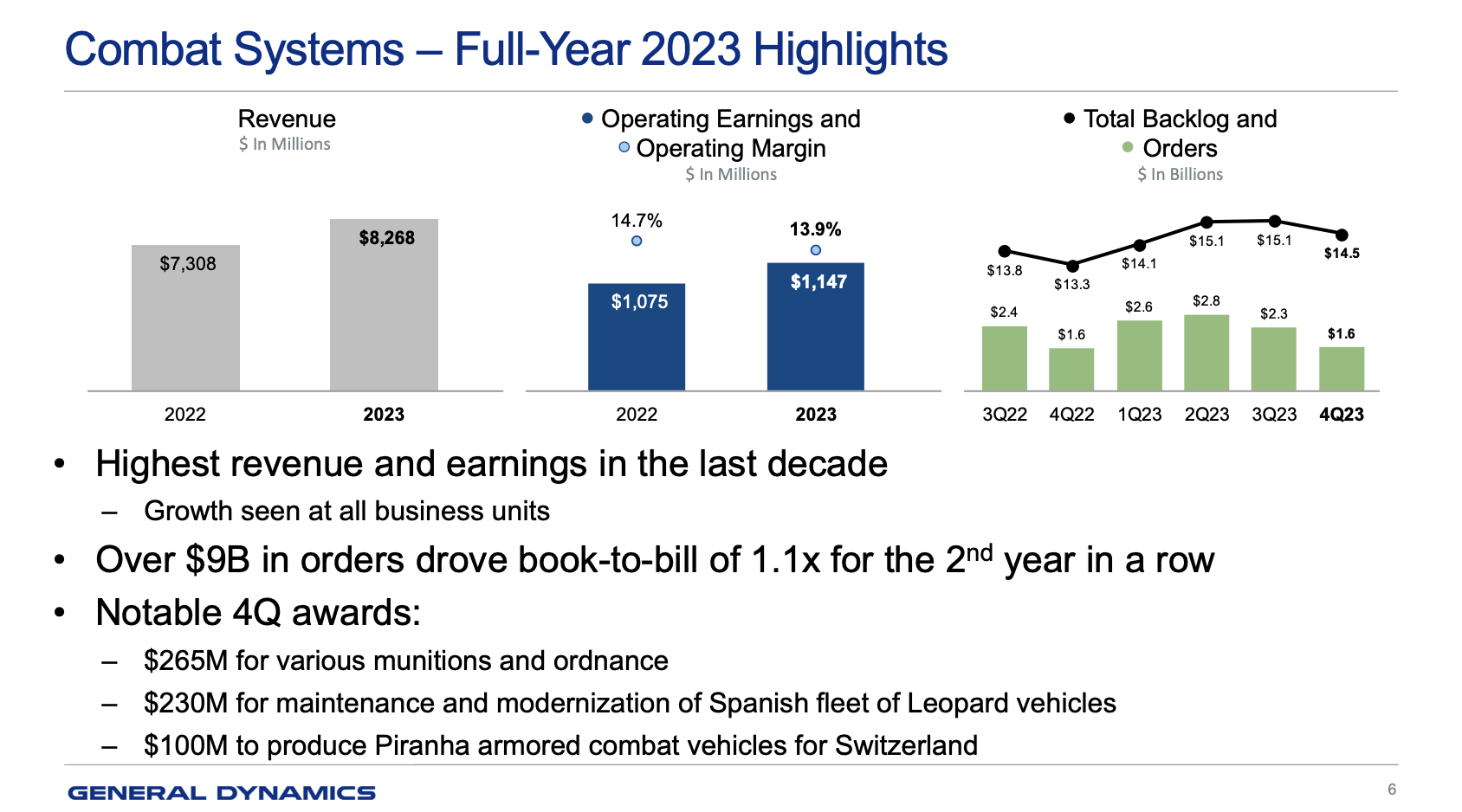

- Combat Systems reported a strong Q4, with an 8.5% increase in revenue compared to the previous year. Operating earnings reached $351 million, reflecting a 5.7% increase on a 40 basis point decrease in operating margin, which still remained robust at 14.8%. Noteworthy growth was seen at Ordnance and Tactical Systems and European Land Systems, primarily driven by higher artillery and propellant volume, as well as expanded production in various programs.

General Dynamics

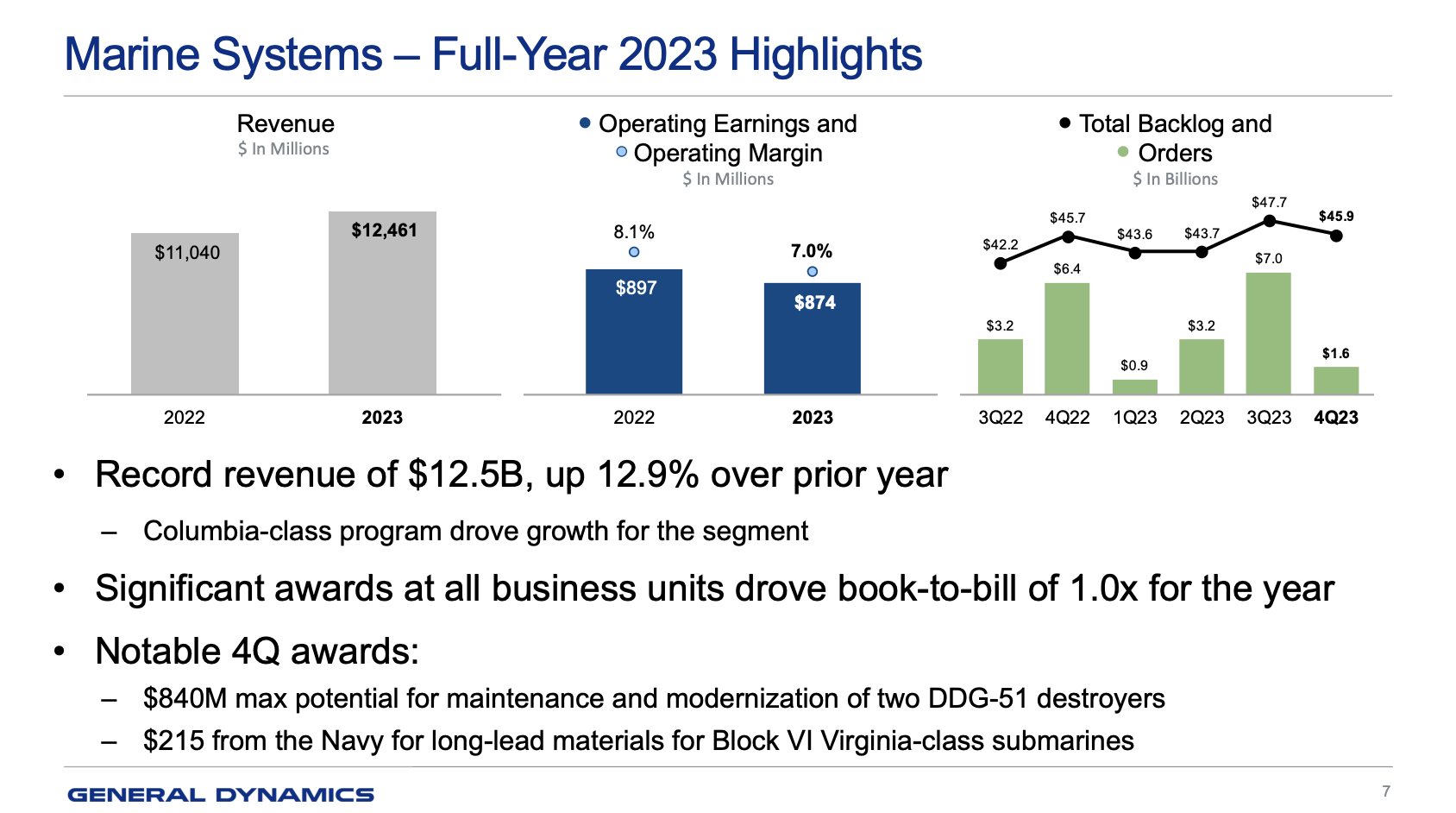

- Marine Systems continued its impressive growth story in Q4, with a 14.8% increase in revenue compared to the previous year. Key drivers included Columbia class construction, TAL volume, and service contracts. However, operating earnings saw an 8.4% decline over the year-ago quarter due to EAC rate decreases at Electric Boat. The challenges included delayed material deliveries to Electric Boat, leading to additional out-of-station work and quality issues from several vendors. Given how capital-intensive Navy operations are, I was not surprised to see this earnings volatility.

General Dynamics

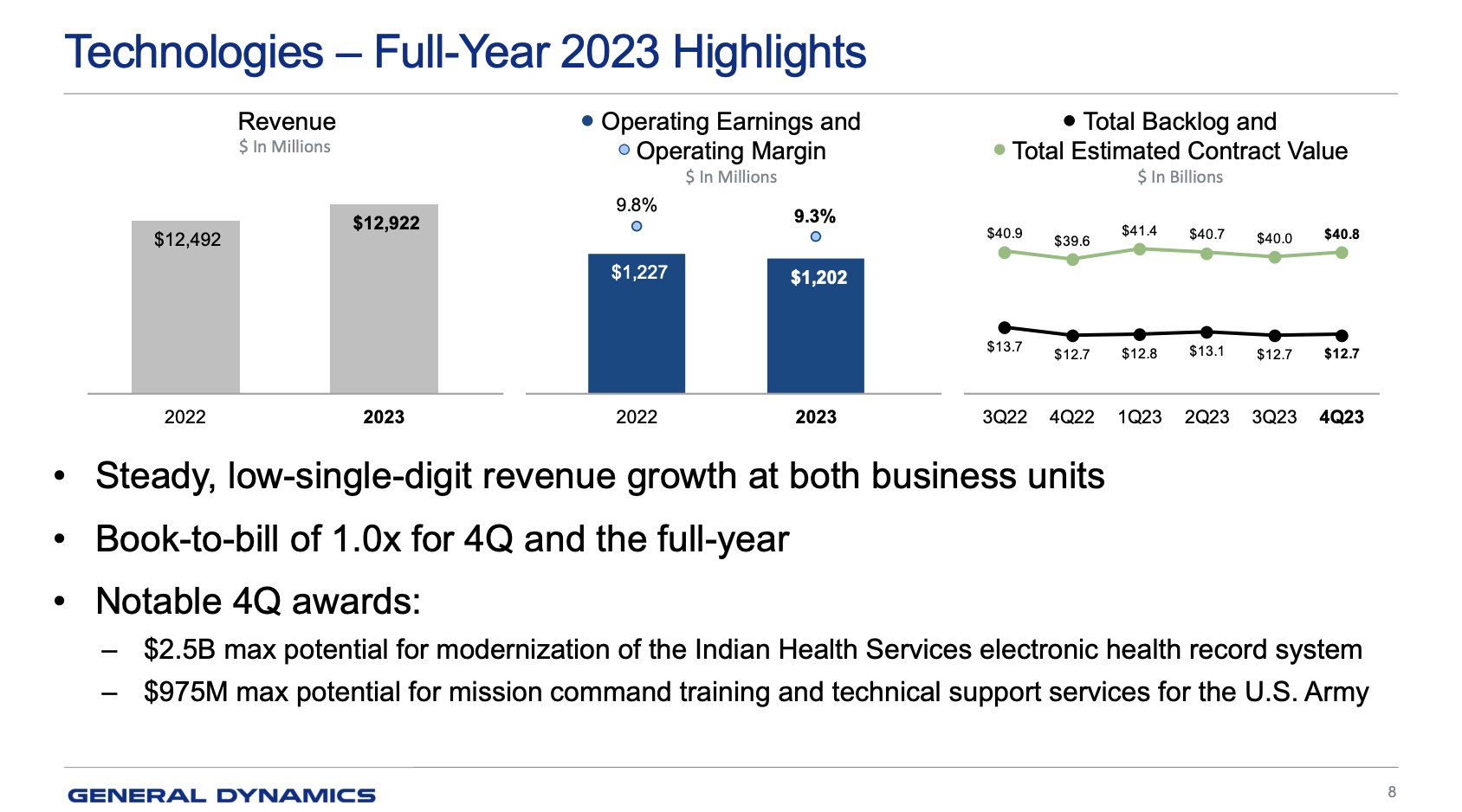

- The Technologies Group reported Q4 revenue of $3.2 billion, representing a 3.1% decrease compared to the prior year. Operating earnings of $305 million were down 10.3% versus Q4 2022. For the full year, however, the group's revenue of $12.9 billion marked a 3.4% increase, exceeding expectations. GDIT within the Technologies Group showcased robust performance, experiencing increased volume across defense, intel, and federal civilian segments.

General Dynamics

Now, let's take a look at its outlook, which, to me, is the most important part of this article - not just because forward-looking statements matter more than past results, but also because the company's comments give us so much intel we can use for other stocks as well.

One Of The Best Environments In Modern History

When it comes to future growth, it's key to monitor total backlog and order growth.

The total backlog at the end of the year reached $93.6 billion, which includes a $2.5 billion increase compared to the previous year.

- The Aerospace segment led with an impressive 1.2x book-to-bill ratio for both the fourth quarter and the full year.

- The Defense segment maintained a 1.0x book-to-bill ratio for the full year.

- Overall, the company achieved a book-to-bill ratio of 1.1x for the year, with all four segments performing at 1x or better.

What this means is that orders are coming in faster than the company can finish its work. A 1.2x B/B ratio implies that for every $1.00 in fished work, the company gets $1.20 in new orders.

This suggests rising revenue in the future.

General Dynamics

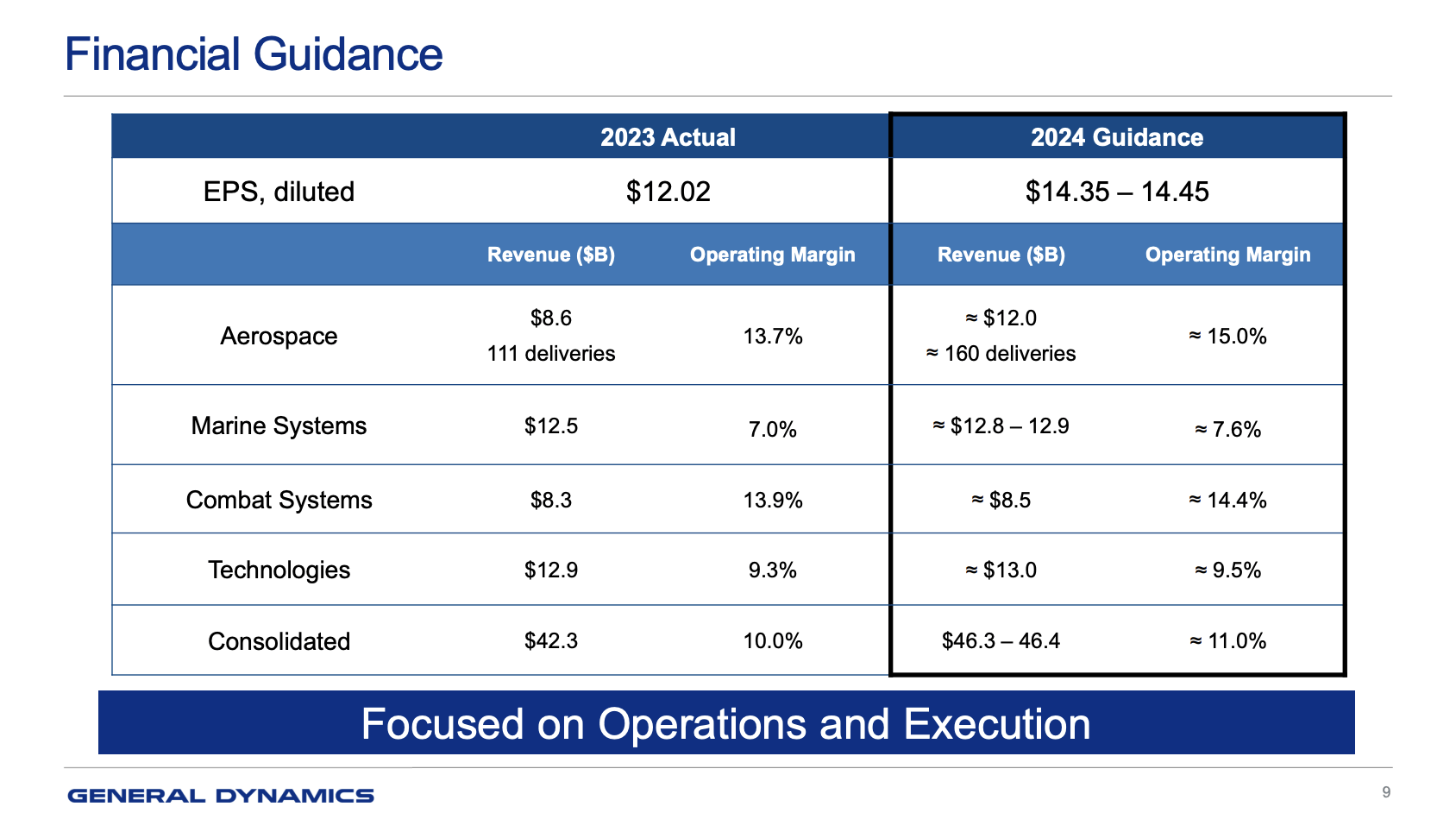

With that in mind, this year's aerospace revenue is projected to be around $12 billion, which implies a 40%(!) increase over 2023.

The operating margin is expected to rise by 130 basis points to 15%.

Gulfstream deliveries are forecasted to be approximately 160, with a mix including 50 G700 deliveries.

Meanwhile, challenges from the Gaza conflicts are impacting the delivery of G280s due to an Israel-based supplier.

At this point, GD is benefitting from both strong demand and fading supply chain issues that have been a drag on operations since the pandemic.

In the Combat Systems segment, 2024 revenue is expected to rise by about 3% to $8.5 billion, accompanied by a 50 basis point improvement in operating margin to 14.4%.

Strong order activity in 2023 and positive demand signals in Europe contribute to the outlook, with potential for additional revenue later in the year, particularly in armaments and munitions.

Also, the way the war in Ukraine is going, I expect that European nations will continue to be huge demand drivers for many more years.

Not only is the Ukraine war turning into a massive artillery battle, but European nations are waking up to the realization they wasted decades not modernizing their armies.

European Defence Agency

According to the European Defence Agency:

• Sweden (+30.1%), Luxembourg (+27.9%), Lithuania (27.6%), Spain (19.3%), Belgium (14.8%) and Greece (13.3%) recorded the highest increases in overall expenditure among the EU 27.

• A record €58 billion was allocated to defence investments; overwhelmingly towards the procurement of new equipment, which increased by 7% on the previous year.

Similar developments are expected in the Marine Group, which builds some of the Navy's largest ships and submarines.

The 2024 outlook for this segment sees revenue of about $12.8 billion and an operating margin of 7.6%, promising meaningful earnings improvement in 2024.

With regard to the Technologies Business Group, for 2024, revenue is expected to increase by about 1% to $13 billion. Within the group, GDIT is expected to see low single-digit growth, while Emission Systems may experience a slight decline due to transitioning from legacy systems and a slow ramp-up on new programs.

Combining all segments, company-wide revenues for 2024 are expected to be approximately $46.3 billion to $46.4 billion, reflecting a 9.5% increase.

- The operating margin is anticipated to reach 11%, up 100 basis points from 2023.

- The earnings per share forecast is around $14.4, with a reasonable range of $14.35 to $14.45.

General Dynamics

In other words, GD is in a fantastic position, as everything seems to go in its favor.

This is how Phebe Novakovic, the company's CEO, put it during the Q4 earnings call (emphasis added):

In summary, as we go into this year, we feel very good about the demand environment across all of our businesses. It has been some time since I have seen stronger demand signals and better promise of organic growth. We also have some very good opportunities across the business to improve operating margins.

So, what does this mean for shareholders?

GD Stock - Shareholder Distributions & Valuation

General Dynamics has a top-tier balance sheet, which helps tremendously when it comes to returning cash to shareholders.

The company finished the year with a cash balance of $1.9 billion and a net debt position of $7.3 billion, representing a substantial reduction of more than 20% from the previous year.

Analysts expect the company to end this year with a net leverage ratio of just 1.1x (EBITDA). It has an A- credit rating, one of the best ratings on the market.

In terms of capital deployment, the company paid $360 million in dividends for the fourth quarter, summing up to $1.4 billion for the year.

Share repurchases consisted of 2 million shares, amounting to $434 million.

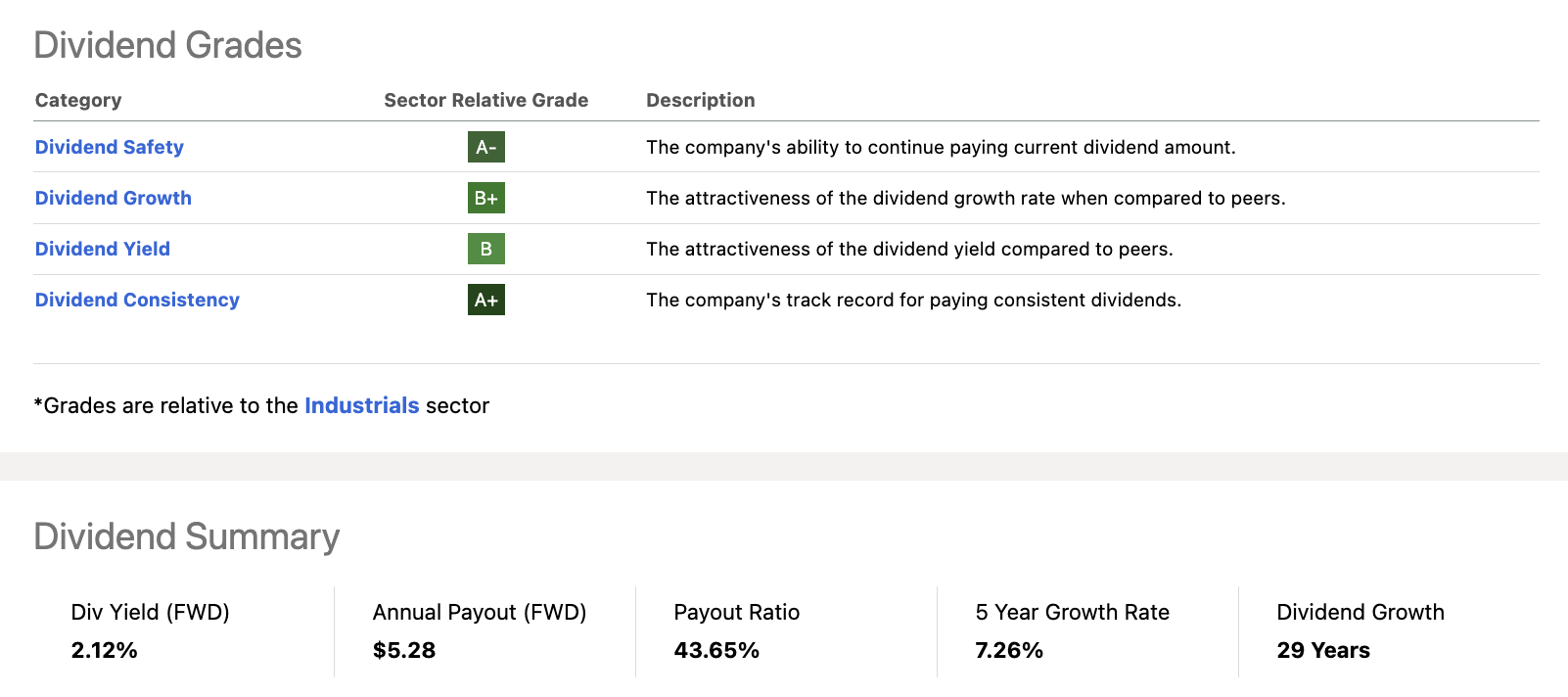

After hiking its dividend by 4.8% on March 9, 2023, it currently pays $1.32 per share per quarter. This translates to a yield of 2.0%.

The five-year dividend CAGR is 7.3%.

Dividends are protected by a healthy balance sheet, a strong business outlook, and a payout ratio in the low-40% range.

Seeking Alpha

The company has hiked its dividend for 29 consecutive years.

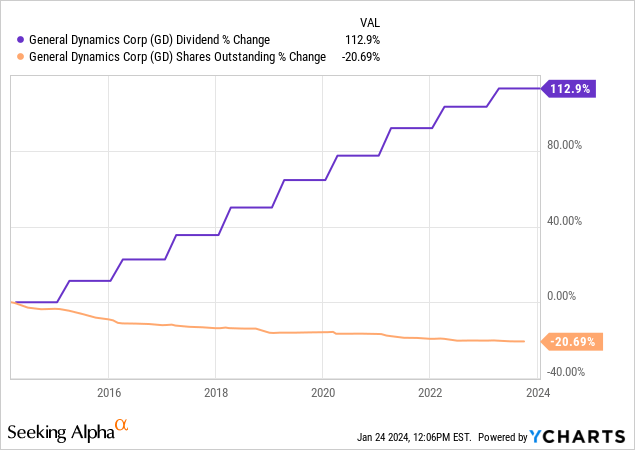

Over the past ten years, its dividend has more than doubled while it bought back a fifth of its shares.

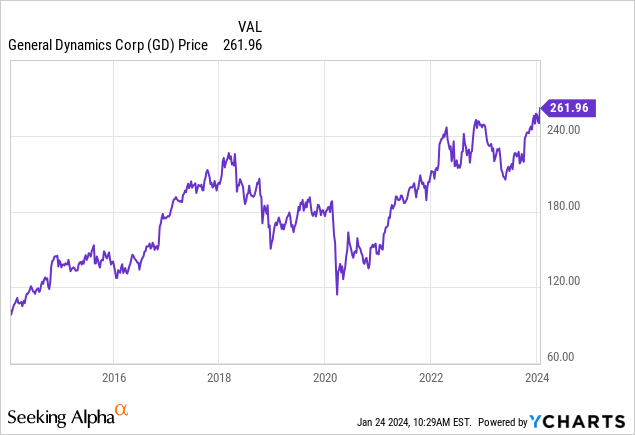

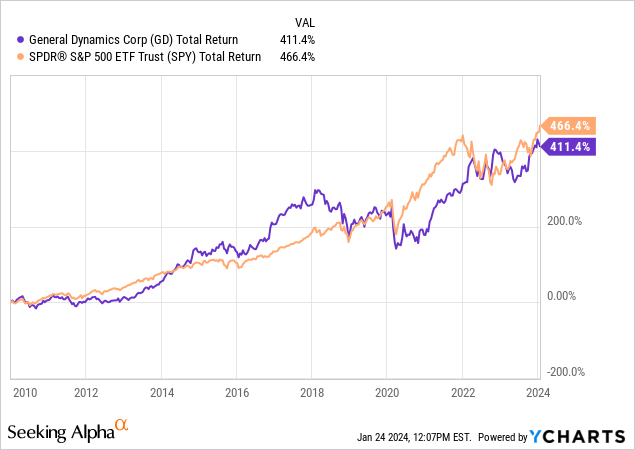

Since 2010, GD shares have returned 411%, failing to outperform the S&P 500.

The failure to outperform the S&P 500 (SP500) mainly came from the aftermath of the global growth peak in 2018 and the pandemic, which ruined the strong performance before 2018 a bit.

Going forward, I expect GD shares to beat the market on a long-term basis.

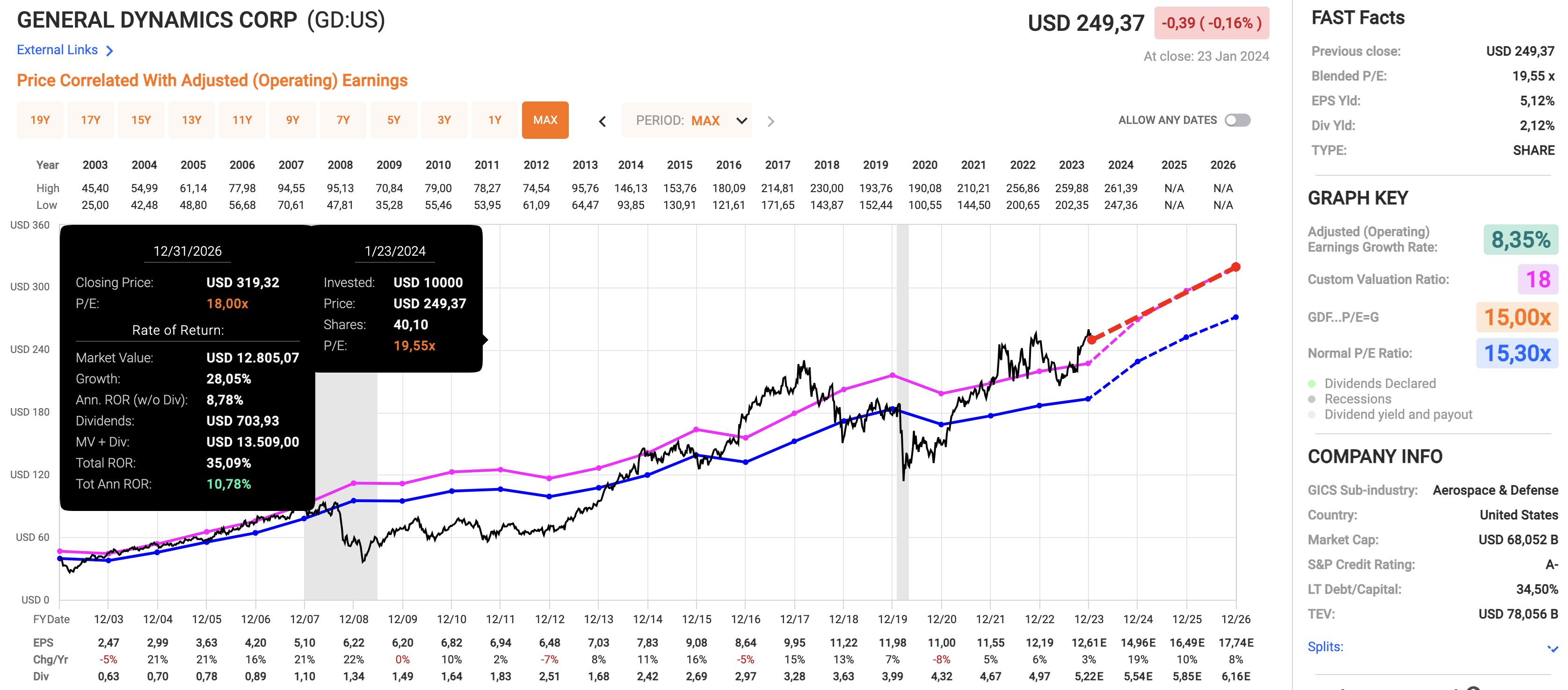

Using the data in the chart below:

- GD trades at a blended P/E ratio of roughly 19.6x.

- Its normalized valuation multiple going back to 2003 is 15.3x.

- I believe an 18x multiple is more appropriate, as it better reflects the company's expected growth trajectory.

- This year, analysts expect the company to grow EPS by 19%, potentially followed by 10% growth in 2025 and 8% growth in 2026.

FAST Graphs

While these numbers are obviously subject to change, they show that GD could return north of 10% per year through 2026.

Since 2003, GD shares have returned 11% per year.

Hence, even after the most recent rally, I still believe that GD shares are worth buying.

Takeaway

General Dynamics shines as an exceptional stock with a robust outlook and compelling growth drivers.

Key growth factors include a substantial backlog of $93.6 billion, a favorable book-to-bill ratio across all segments, and anticipated tailwinds in aerospace, combat systems, and marine group revenues.

Furthermore, amid geopolitical dynamics, GD stands to benefit from increased demand in Europe due to the war in Ukraine.

Meanwhile, shareholders enjoy GD's strong financial position, supported by a top-tier balance sheet, consistent dividend hikes for 29 consecutive years, and share repurchases.

Despite historical fluctuations, GD's forward-looking metrics, including a blended P/E ratio of 19.6x and a projected 19% EPS growth in 2024, position it as an attractive long-term investment with the potential to outperform the market.