Baloncici/iStock Editorial via Getty Images

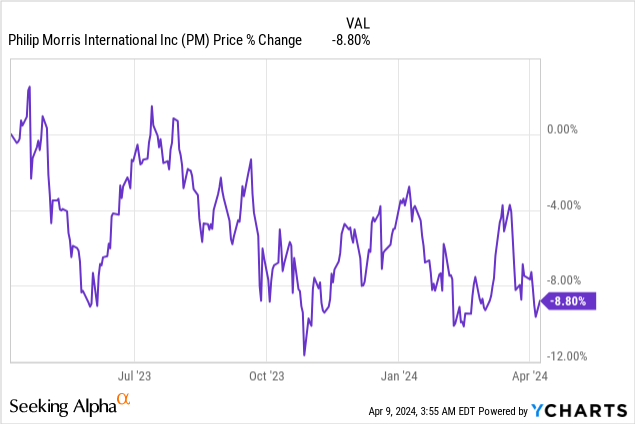

Philip Morris International (NYSE:PM) is a well-run tobacco firm that makes continual gains in the smoke-free product segment. Philip Morris is seeing strong growth for its heated tobacco and electronic cigarette products, and the company has laid out ambitious growth targets to expand its tobacco-free product segments to a two-third revenue share by the end of the decade. Since Philip Morris is growing its profits in the smoke-free segment especially fast, a changing portfolio mix could drive significant income upside for the tobacco company and its shareholders. With a 13X P/E ratio and a 6% dividend yield, I believe the risk profile is attractive for dividend and non-dividend investors alike.

Previous rating

I rated shares of Philip Morris a hold in September 2023 as I believed the growing uptake of the company’s IQOS products was promising, but had reservations about PMI's valuation. IQOS are heated tobacco products that have proven to be very popular with younger users, and the company continued to make strong inroads with this demographic in the last two quarters, adding more than 1M users just in Q4'23. This acceleration of user growth and aggressive revenue targets in the non-traditional product category make shares of Philip Morris an attractive buy for long-term investors that focus on income generation.

Structural portfolio realignment driving growth

Philip Morris is going to rely more and more on non-traditional products such as IQOS to deliver incremental top line and earnings growth in the coming years. With the share of smokers falling consistently for a long time, companies like Philip Morris and Altria Group (MO) are driving innovation in other categories that are meant to offset the decline in traditional tobacco sales. Philip Morris’ non-traditional products include IQOS, e-vapor products as well as ZYN, an oral tobacco pouch brand.

IQOS has been a particular success for Philip Morris because the brand has strong consumer momentum, and it is now generating more than $10.0B in annual revenues. The IQOS brand had close to 29M users at the end of the December quarter, implying that the brand attracted 1.2M more users to its flagship product in the fourth-quarter.

Philip Morris generated a bit more than one-third of its FY 2023 revenues from its smoke-free products, but the tobacco firm expects its portfolio mix to shift in such a way that the company will be able to generate two-thirds of its net revenues from non-traditional products (that is ZYN pouches, e-vapor and IQOS).

Philip Morris

What makes this portfolio realignment especially attractive from a shareholder point of view is that non-traditional products have better unit economics, which in turn implies considerable dividend growth potential for Philip Morris until the end of the decade. According to Philip Morris, the company’s smoke-free products generate 2.6X the gross profit per unit than traditional cigarette sales, which means Philip Morris is set to see profound gross profit and earnings tailwinds as it ramps up the growth of its smoke-free product portfolio. In FY 2023, Philip Morris’ gross profits in the smoke-free segment grew an impressive 19.2% year over year, while its combustible segment gross profits only increased 0.3% year over year.

Philip Morris

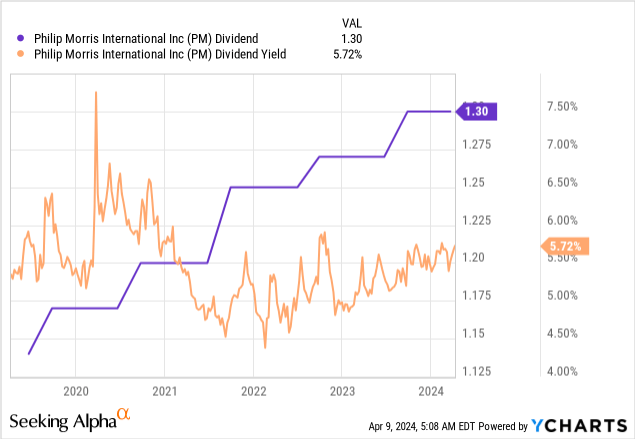

This obviously translates to earnings tailwinds, which may lead to a higher dividend for Philip Morris' shareholders. The tobacco company is growing its dividend each year and has delivered 7.2% annual dividend growth since FY 2008.

Philip Morris’ valuation

The main difference between Philip Morris and Altria is that the latter is concentrated on the U.S. market, while Philip Morris is more internationally oriented and dominating in emerging markets. About 42% of Philip Morris' adjusted net revenues in FY 2023 came from emerging markets, which are also representing stronger growth prospects than the saturated U.S. market.

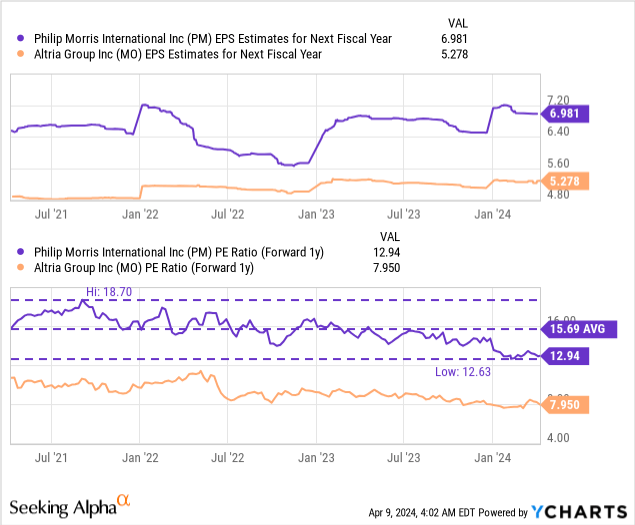

Shares of Philip Morris are valued at a price-to-earnings ratio of 12.9X, compared to Altria’s P/E ratio of 8.0X. The reason why Philip Morris is more expensive relates, in my opinion, to the company's exposure to fast-growing emerging markets, which in turn translates to stronger earnings and EPS growth prospects. Philip Morris is expected to generate 8% annual EPS growth between FY 2024 and FY 2028 while Altria's earnings per-share are projected to grow only at an annual average ratio of 3% during the same time period.

As a result, investors are willing to pay a premium for Philip Morris' shares. Despite its slower growth, I see Altria as a value stock for dividend investors as well, in part because Altria offers a 9.3% dividend, which is even higher than Philip Morris' 6% yield.

Philip Morris was priced at an average P/E ratio of 15.7X in the last three years, and now trades 18% below this average. In my opinion, Philip Morris could easily trade at 15.0X earnings, implying a 7% earnings yield, if the company continues to execute well on its non-traditional product growth plan and keeps growing its IQOS users at a rapid pace. I expect Philip Morris to add at least 2M new IQOS users to its customer base in FY 2024 and continued product/user growth is set to fuel the company's smoke-free segment gross profit momentum... which is why I believe that PMI could revalue to a higher P/E ratio in FY 2024. With a fair value P/E of 15.0X, I believe shares of the tobacco companies could revalue to ~$105, implying 15% revaluation upside.

Risks with Philip Morris

The biggest risk for Philip Morris, as I see it, is potentially a regulatory crackdown on heated tobacco and vape products, which could hurt the company's growth prospects in the smoke-free product category. Litigation is another risk for Philip Morris, as the tobacco industry as a whole has consistently been embroiled in lawsuits relating to the risks of smoking for years. What would change my mind about Philip Morris is if the company saw a deceleration in its smoke-free segment gross profit trajectory.

Final thoughts

Philip Morris is a top income stock for me in FY 2024 and beyond (despite having a lower yield than Altria) as the company executes on its non-traditional product category growth strategy. The tobacco firm saw accelerating user growth for its core IQOS product in the last quarter, and the company now projects that it will be able to derive two-thirds of consolidated revenues from non-traditional product categories by the end of the decade. Philip Morris may not be as cheap as Altria, but the company is expected to grow its earnings faster, which further improves the value proposition for investors that rely on a growing stream of dividend income!